How can ‘blended finance’ help fund climate action and development goals?

Private capital flows to low- and middle-income countries are often constrained by investors’ unfavourable perceptions of risk (actual or perceived). The risks of investing in emerging market range from macro-financial risks (e.g. currency and inflation risk, credit risk) to political and regulatory risks (e.g. laws around investor protection, protection of property rights, unstable legal environments), to technical risks, which are particularly important in large-scale infrastructure projects (e.g. time and cost overruns). The public or philanthropic capital employed in blended finance transactions provides a buffer to such risks, making the investment more attractive to private commercial investors, thereby drawing in private capital that would otherwise not have been available – including finance for achieving climate goals and the Sustainable Development Goals (SDGs).

The success of blended finance rests critically on the ability to maximise additionality, both in terms of the financial resources mobilised and the developmental impact created, while minimising concessionality, i.e. providing public capital at as close to market conditions as possible.

Why might blended finance be needed to help meet climate and development goals?

Progress on achieving the 17 Sustainable Development Goals, including SDG 13 on climate action remains insufficient. In 2015 the annual shortfall in the finance required was US$2.5 trillion and by 2022 this had increased to US$4 trillion For comparison, in 2021 US$178.9 billion of foreign aid was provided by members of the OECD Development Assistance Committee.

Raising the finance to meet climate goals is particularly difficult for low- and middle-income countries. Developed countries committed to channelling US$100 billion per year to developing countries in 2009 but have so far failed to deliver on this promise. This gap in funding climate action is growing: a report published ahead of COP27 suggested that the investment needs for climate action alone in emerging markets and developing countries (other than China) total US$1 trillion per year.

The political nature of development assistance and the budgetary implications for donor countries mean that these financing gaps cannot be closed through increased aid alone. In international fora such as the G20 UN institutions the Organisation for Economic Co-operation and Development and the International Energy Agency, as well as in development finance institutions (DFIs), ‘blended finance’ is viewed as a promising tool to bridge the SDG and climate financing gaps by mobilising private sector investment.

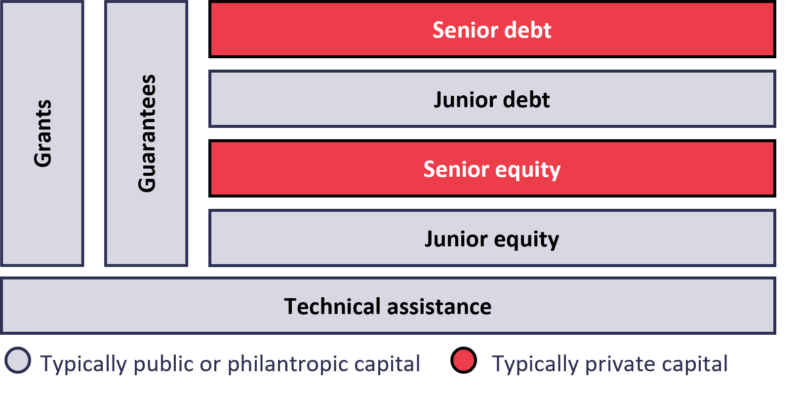

Figure 1. Common instruments used in blended finance transactions

There are several ‘instruments’ used in blended finance transactions, as shown in Figure 1 and described below.